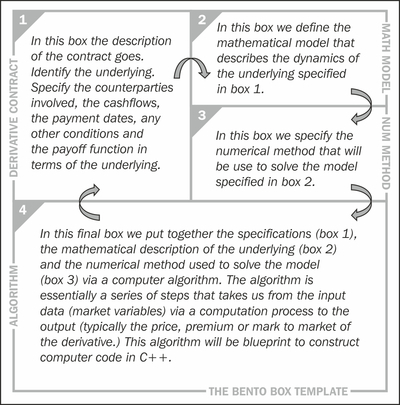

A Bento Box is a single portion take-away meal common in Japanese cuisine. Usually, it has a rectangular form that is internally divided in compartments to accommodate the various types of portions that constitute a meal. In this book, we use the metaphor of the Bento Box to describe a visual template to facilitate, organize, and structure the solution of derivative problems. The Bento Box template is simply a form that we will fill sequentially with the different elements that we require to price derivatives in a logical structured manner. The Bento Box template when used to price a particular derivative is divided into four areas or boxes, each containing information critical for the solution of the problem. The following figure illustrates a generic template applicable to all derivatives:

The Bento Box template – general case

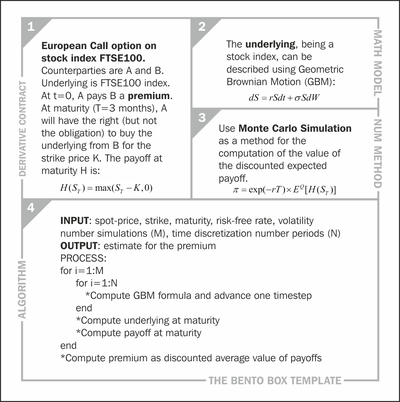

The following figure shows an example of the Bento Box template as applied to a simple European Call option:

The Bento Box template – European Call option

In the preceding figure, we have filled the various compartments, starting in the top-left box and proceeding clockwise. Each compartment contains the details about our specific problem, taking us in sequence from the conceptual (box 1: derivative contract) to the practical (box 4: algorithm), passing through the quantitative aspects required for the solution (box 2: mathematical model and box 3: numerical method).