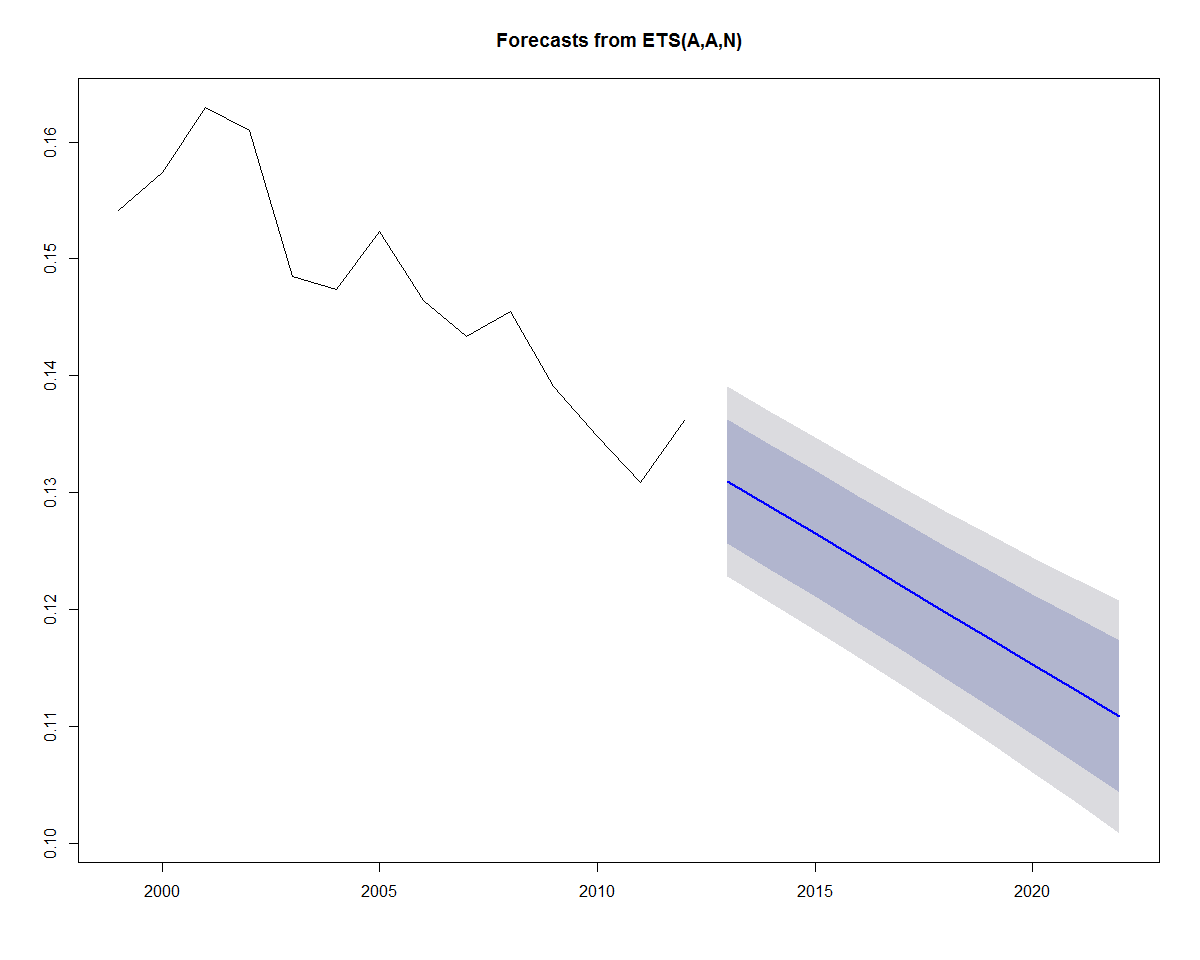

Earlier, we added a linear trend line to the data. If we wanted to incorporate a linear trend into the forecast as well, we can substitute A for the second parameter (trend parameter), which yields an "AAN" model (Holt's linear trend). This type of method allows exponential smoothing with a trend:

fit <- ets(x, model = "AAN") summary(fit) > ETS(A,A,N) > > Call: > ets(y = x, model = "AAN") > > Smoothing parameters: > alpha = 0.0312 > beta = 0.0312 > > Initial states: > l = 0.1641 > b = -0.0021 > > sigma: 0.0042 > > AIC AICc BIC > -108.5711 -104.1267 -106.0149 > > Training set error measures: > ME RMSE MAE MPE MAPE > Training set -0.000290753 0.004157744 0.003574276 -0.2632899 2.40212 > MASE ACF1 > Training set 0.7709083 0.05003007

Plotting the forecast yields the plot below:

plot(forecast(fit))