The general rule of thumb for changing frequency can be broken down into the following:

- Multiply/divide the log returns by the number of time periods.

- Multiply/divide the volatility by the square root of the number of time periods.

In this recipe, we present an example of how to calculate the monthly realized volatilities for Apple using daily returns and then annualize the values.

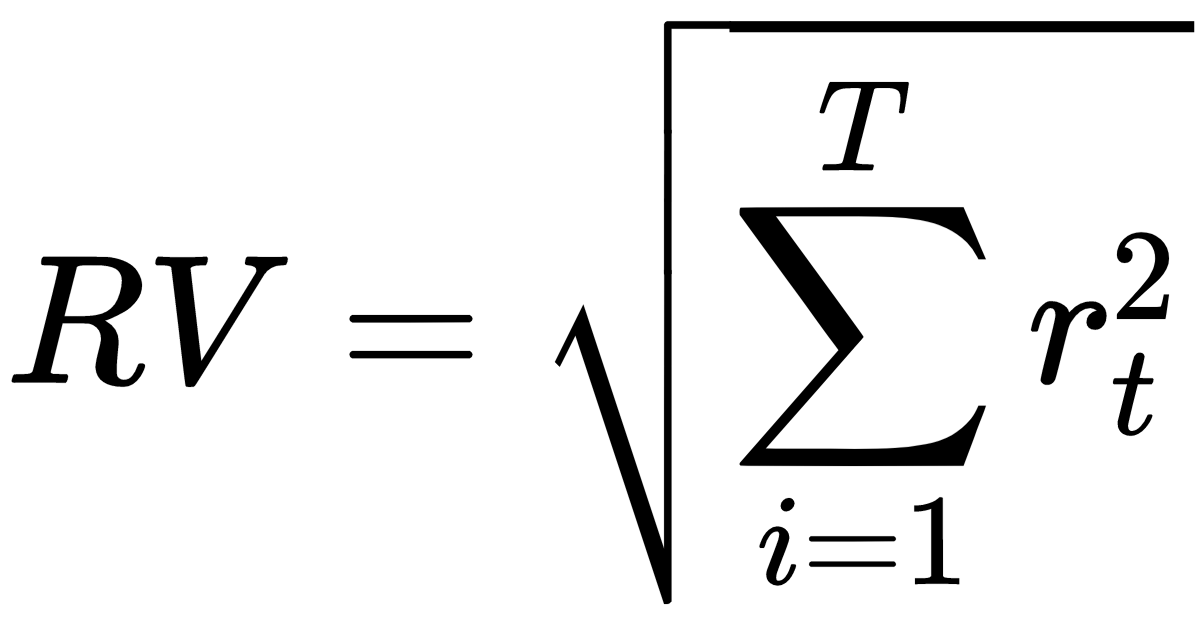

The formula for realized volatility is as follows:

Realized volatility is frequently used for daily volatility using the intraday returns.

The steps we need to take are as follows:

- Download the data and calculate the log returns.

- Calculate the realized volatility over the months.

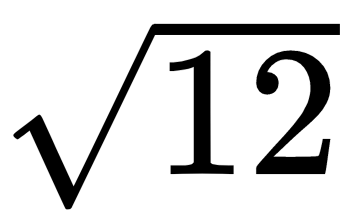

- Annualize the values by multiplying by

, as we are converting from monthly values.

, as we are converting from monthly values.